Offering financing for your customers gives them the opportunity to make the best buying decision for their home, investment, and their budgets. In this article, we’ll discuss:

Home improvement financing is a way for homeowners to access the funds they need for repairs and renovations. Often, homeowners access financing because they don’t have the money to pay for their project at the moment or they would like to not dip into their savings to pay for a project outright. Instead, homeowners can choose financing options because it helps them keep their cash on hand in case anything else happens.

Home equity lines of credit (HELOCs), home equity loans, and secured loans all work similarly. You put up an asset like your home, car, or boat, and the lender loans you money based on the value of that asset, your credit history, and other factors.

HELOCs are unique because, instead of a lump sum of money, a lender will open a line of credit for a specific amount you can draw funds from.

The most significant benefit of secured loans is that lenders tend to offer lower rates for secured loans because if you default on your loan, they can seize your asset.

However, this means that your home or whatever assets you put up for a secured loan are the risk you’re using as collateral.

Unsecured personal loans don’t use collateral or assets to determine the amount you can receive from a lender or the rate. This type of loan’s principal, interest rate, and terms are mostly determined by credit history, debt-to-income ratios, and FICO score.

Because this type of financing does not require collateral, the rates and the loan terms (the amount of time you have to pay the loan back) are different from secured loans. APRs tend to be higher and loan terms tend to be shorter.

Credit cards are a ubiquitous way to purchase goods and services in American life. Similar to unsecured loans, the credit limit and APR for a borrower are determined by credit score, history, and debt-to-income ratio.

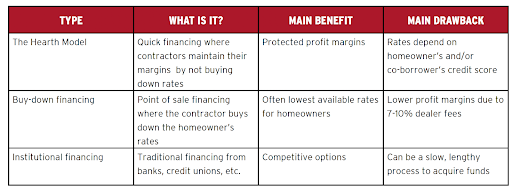

For a few decades, home improvement contractors have offered financing options to their customers for their projects. As the years moved forward, the process became simpler and simpler. Now, instead of using a paper form and snail mail, customers can use services like Hearth to find monthly payment options quickly and easily via a prequalification form. However, you should know the different types of financing programs so you can make the right decision for your company.

This type of financing relies on the typically slow processes associated with banks and big lenders. There are long application processes and waiting times. This type of financing institution usually works directly with the homeowners, which means you don’t receive status updates on their progress or when they receive their funds.

Buy-down financing programs are how home improvement and services contractors have traditionally offered monthly payment options to their customers. Buy-down financing works like this: you secure the job, you and the client agree on an amount, they request financing, and the contractor or business has to pay a percentage of the loan amount to buy down the APR on behalf of the customer. No matter what APR you buy down to, you’re on the hook for a percentage of the job.

That means if you want to offer financing to any of your customers, you will have to pay a per-project fee or dealer fee. This means you’ll likely have to raise your prices to protect your profits from these fees eating into your margins. Fees can range from 7–10%.

Not only that, many of these lending programs have time-in-business requirements, revenue requirements, or will run your business’ credit history. Even if you wanted to use their services, you might not qualify. Also, some of these programs require disbursements or customer approval to release funds to your account. Finally, some of them only work with customers who have premium credit scores.

The Hearth model has been copied and refabricated by competitors, but Hearth is still the leader in home improvement financing. Our tool gives contractors the ability to send a prequalification form via text or email to their customers. From there, the customers fill out the form to see their estimated monthly payment options. When the customer chooses their favorite option, they apply for that loan through the lending institution. If they are approved, they get their cash to pay for your project.

With Hearth, there are no minimum requirements to offer financing to your customers.

We have a marketplace of up to 17 different lenders ready to connect your customers to financing for their projects. And, they are ready to work with customers that have FICO scores as low as 550, for projects as high as $250,000, and loan terms as long as 12 years. Also, your customers’ credit scores aren’t affected when they use the prequalification form to see their estimated monthly payments.

Best of all, there are no per-project fees for contractors, and you’re not penalized for your success.

Financing for restoration projects is simple. Similarly to roofing projects, your customers have insurance claims and deductibles to deal with, and their health and safety are likely their first priority. They likely just want their projects done.

Sometimes you don’t want to wait for the insurance company to cut a check. Some homeowners will finance a job, get the funds, pay for the job, and then reimburse themselves with the funds they receive from their insurance company.

Sometimes families and property owners don’t have the cash for unexpected repair or deductible costs. Financing is a great way to get the job they need completed while protecting whatever cash they have in savings or by building the costs into their monthly budgets.

Let’s face it. Sometimes insurance doesn’t cover everything, especially if the homeowner has an actual cash value (ACV) plan. Financing helps cover the rest by providing quicker access to cash than traditional financing sources, including secured loans.

We suggest offering financing as early as possible. Mention financing options in your marketing pieces like direct mail or on your website. Social media is a great place to announce you can offer monthly payment options.

We also suggest including it in your appointment materials and email signatures. And, bring it up early in the sales conversation, like the example below.

Sometimes the money conversation can feel uncomfortable when you’re trying to close the deal. However, offering financing as part of your payment options can give you more confidence to discuss money with your customers. When talking price, bring up the multiple payment options you have.

“Before we talk about the specifics, I want to let you know some of my customers pay using monthly payments, and others use cash. If you’re interested in paying for the project over time, Hearth can help you see payment options without affecting your credit score.”

If they say they will pay in cash…

“Great! Let me know if you want to see monthly payments at any time. Seeing options doesn’t affect your credit score and monthly payments can help you upgrade part of your project.”

We’ve broken down financing for restoration pros in the article above, but don’t take our word for it. Here is a story from a real Hearth customer on how they use Hearth to win more jobs.

Customers complete a short online financing request and can get immediately pre-qualified by up to 17 lending partners without affecting their credit score.

Contractors find customized payment plans for each customer. They can offer financing before an on-site visit, in the home, or as a follow-up.

Customers apply for their preferred loan option and if approved, receive funding in as few as 24 hours.